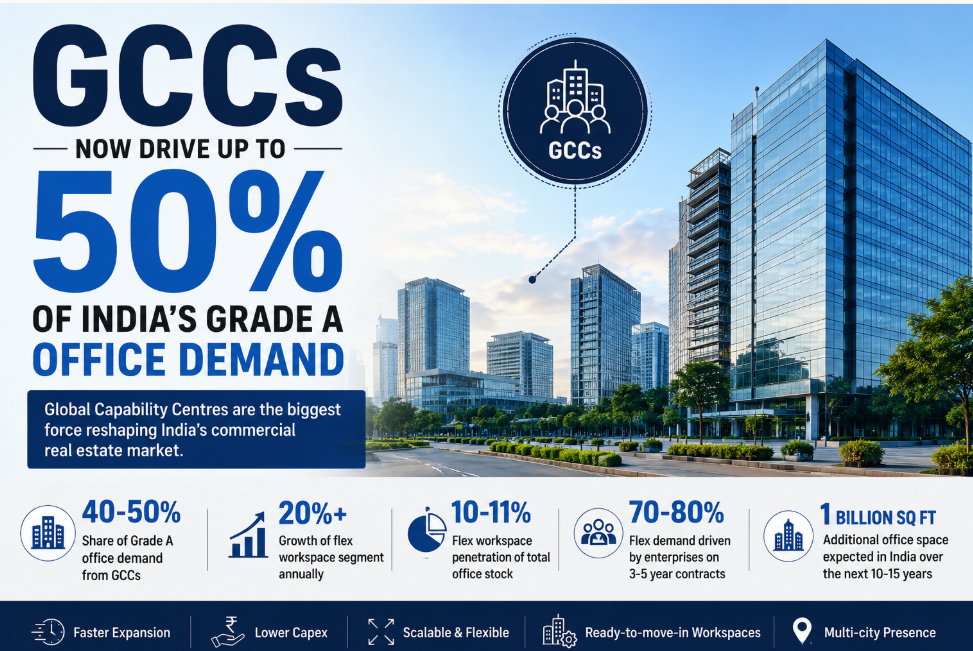

For years, India’s office market moved in lockstep with the fortunes of the IT services industry. Whenever technology hiring surged, office leasing followed. But a quiet transformation is underway. Global Capability Centres (GCCs) have emerged as the single biggest force shaping India’s commercial real estate landscape, accounting for nearly 40-50 per cent of all Grade A office demand in the country.

The shift marks a fundamental change in the way multinational corporations view India. No longer merely a low-cost outsourcing destination, India has become a strategic hub for engineering, research and development, artificial intelligence, finance, cybersecurity, data analytics, product design, and digital transformation.

As global companies expand their India operations, GCCs are becoming the primary occupiers of premium office space, influencing everything from rental growth and vacancy levels to the rise of flexible workspaces.

New Occupiers of Corporate India

The numbers tell a compelling story. According to Smartworks Coworking Spaces, GCCs now contribute 40-50 per cent of Grade A office demand in India. At the same time, demand from these centres for flexible workspaces is expected to double over the next two years.

This surge comes as the country continues to attract multinational corporations looking to establish global back offices, innovation centres, and technology hubs. From Fortune 500 companies to emerging global enterprises, firms are increasingly choosing India to house critical business functions.

GCCs Reshape India’s Office Market

Global Capability Centres (GCCs) now account for 40-50% of Grade A office demand in India, making them the single biggest force driving the country’s commercial real estate market. As multinational companies expand their India operations, GCCs are increasingly influencing office leasing, rental growth, workplace design, and the rapid adoption of flexible workspaces across major business hubs.

Industry estimates suggest India hosts more than 1,800 GCCs employing millions of professionals. The country is rapidly evolving into the world’s largest GCC destination, supported by a deep talent pool, favourable costs, digital infrastructure, and a thriving startup ecosystem.

Office Demand Gets a New Engine

The rise of GCCs has come at an important time for India’s office market. India’s commercial office market currently spans nearly one billion square feet. While the sector has expanded steadily at around 8 per cent annually, flexible workspaces have been growing at more than 20 per cent a year, making them the fastest-growing segment within commercial real estate. At the same time, supply is tightening.

The supply-to-demand ratio in India’s Grade A office market has fallen dramatically from 1.02 times in 2021 to just 0.5 times in 2025. Vacancy levels have dropped to decade lows, while rentals are rising across major office markets.

The result is a landlord’s market where premium office space is becoming increasingly scarce.

“GCC demand is no longer incremental. It is becoming the dominant force behind office absorption in India’s leading business districts,” says a commercial real estate consultant tracking the sector.

Why GCCs Prefer Flexibility

Unlike traditional corporate occupiers, GCCs often scale rapidly and need the ability to add thousands of employees within short periods. This has created a growing preference for managed office spaces and flexible campuses.

The flex workspace industry, once associated with startups and freelancers, has undergone a significant transformation. Today, 70-80 per cent of flex demand comes from enterprises signing long-term contracts of three to five years.

Smartworks, India’s largest managed campus platform, says enterprises are increasingly using flex offices as a core part of their workplace strategy rather than as temporary overflow space. The company manages more than 16 million square feet across 66 campuses and 15 cities.

The attraction is clear. Managed office operators can provide ready-to-occupy workplaces within weeks rather than months, allowing GCCs to expand quickly without committing large capital investments toward fit-outs and infrastructure.

Beyond Bengaluru

While Bengaluru remains India’s GCC capital, the expansion is becoming more geographically diversified. Hyderabad, Pune, Chennai, Gurugram, Noida and Mumbai continue to attract new centres, while a growing number of multinational companies are evaluating tier II cities to access talent and reduce costs. This trend could significantly broaden the economic impact of GCC investments across the country. For office developers, the implication is clear: future demand will increasingly be linked to where GCCs choose to locate and expand.

The Next Decade for GCCs

The long-term opportunity remains enormous. The country is expected to add another one billion square feet of office space over the next 10 to 15 years. Meanwhile, flex workspace penetration, currently at around 10-11 per cent of total office stock, is expected to double. As multinational corporations continue to shift strategic functions to India, GCCs are likely to remain the single largest source of new office demand. The impact extends far beyond commercial real estate. GCC expansion drives employment, supports urban infrastructure development, boosts public transport utilisation, and creates demand for housing, retail and hospitality services.

For office developers, landlords, REITs and workspace operators, the message is unmistakable. The future of India’s commercial real estate market will increasingly be written by GCCs. What began as a back-office revolution has evolved into a real estate revolution. And India’s Grade A office market is now one of its biggest beneficiaries.

Key Takeaways

- GCCs account for 40-50% of India’s Grade A office demand.

- GCC demand for flexible workspaces is expected to double within two years.

- India’s office market spans nearly 1 billion sq ft.

- Flex workspaces are growing at more than 20% annually, versus 8% growth in the overall office market.

- Grade A office supply is tightening, with vacancy at decade lows.

- India is expected to add another 1 billion sq ft of office space over the next 10-15 years.

Source: Centrum Institutional’s Nakshatra The Shining Stars Investor Conference Report, Smartworks Coworking Spaces section.