For generations, the real estate business has revolved around a familiar mantra: location, location, location. The value of an office tower, shopping mall or residential complex is largely determined by where it stands and how efficiently the space can be monetised.

Data centres operate by a very different logic.

While they are often grouped under the real estate umbrella, the economics of a modern data centre are fundamentally driven by infrastructure rather than built space. The land and the building may provide the shell, but the real value lies in the electrical systems, cooling architecture and engineering capabilities that keep servers running around the clock.

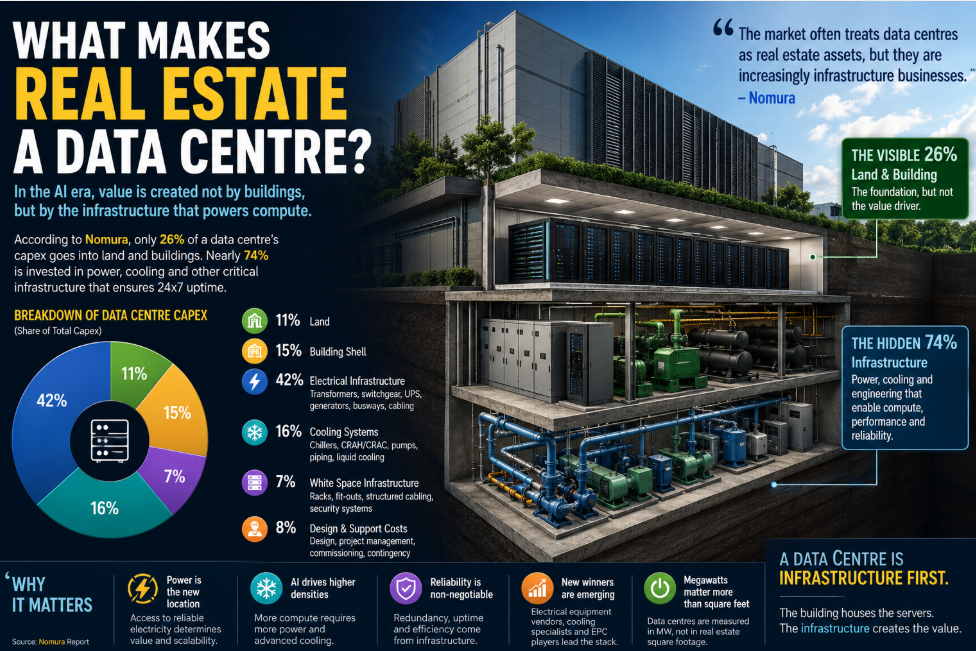

“The market often treats data centres as real estate assets, but they are increasingly infrastructure businesses,” says Nomura in a recent report. The brokerage notes that only about a quarter of a data centre’s capital expenditure is allocated to land and buildings, while nearly three fourths is spent on power delivery, cooling systems and other compute enabling infrastructure.

That distinction is becoming even more important as artificial intelligence reshapes the global digital economy.

The Anatomy of a Modern Data Centre

Hover over each component to explore its role in the data centre ecosystem.

🏢 Real Estate

26%⚡ Infrastructure

74%Beyond Bricks and Mortar

According to Nomura, the real estate layer accounts for just 26 per cent of a typical data centre’s capex stack. Land represents around 11 per cent of total investment, while the base building and shell contribute another 15 per cent.

The remaining 74 per cent is dedicated to infrastructure.

Electrical systems alone account for around 42 per cent of total capex. These include transformers, switchgear, UPS systems, backup generators, busways and cabling networks designed to ensure uninterrupted power delivery. Mechanical and cooling infrastructure contributes another 16 per cent, while white space fit outs, structured cabling, security systems and project management make up the balance.

In other words, a data centre is less comparable to an office complex and more akin to a power intensive utility asset.

The AI Effect

Artificial intelligence is accelerating this shift.

Traditional enterprise workloads could operate comfortably within relatively modest power envelopes. AI workloads are different. Training and running large language models requires significantly greater computing density, resulting in far higher power consumption and heat generation.

As rack densities rise, operators are investing in advanced cooling technologies, including liquid cooling systems that can efficiently manage next generation AI servers. Higher uptime requirements are also driving additional spending on power redundancy and backup systems.

This means that every new AI ready facility contains a larger share of infrastructure investment than the generation before it.

“The infrastructure share of capex continues to rise as workloads become more compute intensive,” Nomura notes, pointing to growing requirements for high density deployments, liquid cooling and stricter uptime standards.

Following the money

The implications extend well beyond data centre operators.

If most of the investment in a data centre is flowing into power and cooling infrastructure, then much of the value creation is likely to accrue to the companies supplying those systems.

Nomura argues that the biggest beneficiaries of the data centre buildout may increasingly be electrical equipment manufacturers, cooling solution providers and engineering, procurement and construction companies rather than traditional real estate developers.

The beneficiaries of the AI boom, therefore, may not simply be those who own the buildings. They may be the companies supplying transformers, switchgear, generators, cooling systems and power management solutions that make those buildings functional.

From Square Feet to Megawatts

The transformation is also changing how data centres are valued.

Commercial real estate is typically measured in terms of occupancy rates, rental yields and returns per square foot. Data centres are increasingly evaluated on metrics such as power capacity, energy efficiency, uptime and megawatt availability.

A site with access to substantial electrical capacity may command a premium even if its physical footprint is relatively modest. Conversely, a large parcel of land without adequate power infrastructure may have limited strategic value.

As a result, the industry’s most critical question is no longer how much space is available, but how much power can be delivered.

A New Asset Class

The rise of AI is blurring the traditional boundaries between real estate and infrastructure. While data centres continue to sit on valuable land and occupy large buildings, their economics are increasingly defined by power networks, cooling systems and engineering complexity.

The building may house the servers, but it is the infrastructure that creates the value.

Perhaps that is the clearest answer to the question: What makes real estate a data centre?

Not the walls. Not the land. Not even the building itself. It is the ability to convert electricity into computation at scale.