Dell Technologies delivered a blockbuster first quarter for fiscal 2027, powered by an unprecedented surge in artificial intelligence infrastructure demand. During the earnings call, management highlighted record revenue of $43.8 billion, up 88% year-on-year, while diluted earnings per share jumped 214% to a record $4.86. The company credited the performance to strong execution across its AI, server, storage and PC businesses.

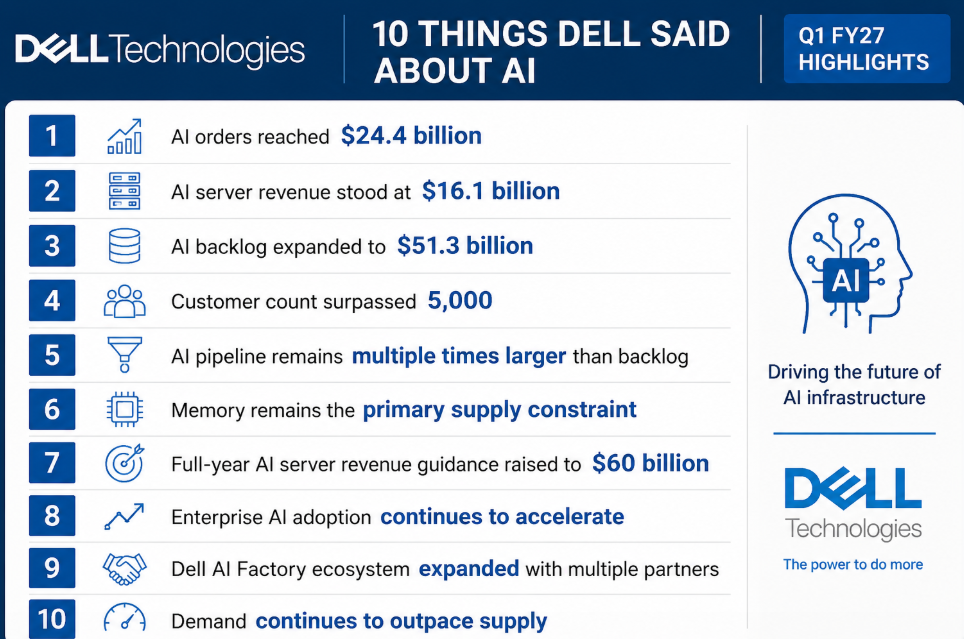

AI emerged as the biggest growth engine for Dell. The company reported AI orders worth $24.4 billion during the quarter and recognized $16.1 billion in AI server revenue. Dell exited the quarter with a record AI backlog of $51.3 billion, while management said its pipeline continues to grow and remains several times larger than the existing backlog. According to executives, demand continues to exceed supply, with memory availability remaining the primary constraint.

Dell also emphasized the rapid expansion of its AI ecosystem. The company is extending its AI Factory strategy from data centres to enterprise desktops and edge environments through partnerships with NVIDIA, Google Cloud, OpenAI, Palantir, ServiceNow, Mistral and others. Management noted that enterprises are increasingly moving from AI pilots to production deployments, creating demand not only for AI servers but also for traditional compute, storage and networking infrastructure.

Looking ahead, Dell raised its full-year fiscal 2027 outlook and now expects approximately $60 billion in AI server revenue. Executives repeatedly stressed that demand across AI, traditional servers, storage and PCs is accelerating rather than slowing, with supply constraints, not customer demand, emerging as the biggest challenge. The following is the full transcript of Dell Technologies’ Q1 FY27 earnings conference call held on May 28, 2026.

Dell Technologies Q1 FY27 Earnings Call Transcript

Page 1

May 28, 2026 / 9:30PM, DELL – Q1 2027 Dell Technologies Inc Earnings Call

TRANSCRIPT

DELL – Q1 2027 Dell Technologies Inc Earnings Call

EVENT DATE/TIME May, 28 2026 9:30PM GMT

Page 2

May 28, 2026 / 9:30PM, DELL – Q1 2027 Dell Technologies Inc Earnings Call

C O R P O R A T E P A R T I C I P A N T S

Paul Frantz Dell Technologies Inc – Head of Investor Relations

Jeff Clarke Dell Technologies Inc – Vice Chairman and Chief Operating Officer

David Kennedy Dell Technologies Inc – Chief Financial Officer

C O N F E R E N C E C A L L P A R T I C I P A N T S

Ben Reitzes Melius Research LLC – Equity Analyst

Mark Newman Sanford C Bernstein & Co LLC – Analyst

Amit Daryanani Evercore Inc – Equity Analyst

Wamsi Mohan Bofa Merrill Lynch Asset Holdings Inc – Analyst

Katherine Campagna Goldman Sachs – Analyst

Samik Chatterjee JPMorgan Chase & Co – Analyst

Asiya Merchant Citibank Cameroon SA (Douala Branch) – Analyst

Erik Woodring Morgan Stanley – Analyst

David Vogt UBS AG – Analyst

Tim Long Barclays Services Corp – Equity Analyst

Simon Leopold Raymond James Inc – Analyst

Krish Sankar Cowen and Company LLC – Analyst

P R E S E N T A T I O N

Operator: Good afternoon, and welcome to the Fiscal Year 2027 First Quarter Financial Results Conference Call for Dell Technologies Inc. I’d like

to inform all participants this call is being recorded at the request of Dell Technologies. This broadcast is the copyrighted property of Dell

Technologies Inc. Any rebroadcast of this information in whole or part without the prior written permission of Dell Technologies is prohibited.

Following prepared remarks, we will conduct a question-and-answer session. (Operator Instructions)

I’d like to turn the call over to Paul Frantz, Head of Investor Relations. Mr. Frantz, you may begin.

🔹 10 Things Dell Said About AI

- ✅ AI orders reached $24.4 billion

- ✅ AI server revenue stood at $16.1 billion

- ✅ AI backlog expanded to $51.3 billion

- ✅ Customer count surpassed 5,000

- ✅ AI pipeline remains multiple times larger than backlog

- ✅ Memory remains the primary supply constraint

- ✅ Full-year AI server revenue guidance raised to $60 billion

- ✅ Enterprise AI adoption continues to accelerate

- ✅ Dell AI Factory ecosystem expanded with multiple partners

- ✅ Demand continues to outpace supply

Paul Frantz – Dell Technologies Inc – Head of Investor Relations

Thanks, everyone, for joining us. With me today are Jeff Clarke, David Kennedy and Tyler Johnson. Our earnings materials are available on our IR website, and I encourage you to review these materials. Also, please take some time to review the presentation, which includes additional content to complement our discussion this afternoon. During this call, unless otherwise indicated, all references to financial measures refer to

non-GAAP financial measures, including non-GAAP gross margin, operating expenses, operating income, net income diluted earnings per share,

free cash flow and adjusted free cash flow.

A reconciliation of these measures to their most directly comparable GAAP measures can be found in our web deck and our press release.

Growth percentages refer to year-over-year change unless otherwise specified. Statements made during this call that relate to future results and

events are forward-looking statements based on current expectations. Actual results and events could differ materially from those projected due

to a number of risks and uncertainties, which are discussed in our web deck and our SEC filings. We assume no obligation to update our forward-

looking statements.

Now I’ll turn it over to Jeff.

Jeffrey Clarke – Dell Technologies Inc – Vice Chairman and Chief Operating Officer

Thanks, Paul, and thanks, everyone, for joining us. What a great start to FY27. The first quarter underscored the strength and agility of our

operating model and the advantage of our broad portfolio. Our team executed very well in a challenging environment, delivering record

revenue and EPS. Revenue was $43.8 billion, up 88% and earnings per share was $4.86, up 214%.

Page 3

May 28, 2026 / 9:30PM, DELL – Q1 2027 Dell Technologies Inc Earnings Call

Demand was stronger than we anticipated across all lines of businesses and geographies with customers moving decisively to secure supply

across a broad range of IT needs. This drove meaningful scale, record cash generation and continued strong capital returns for shareholders. Our

strong performance reflects not only demand in the quarter, but also the pace of innovation we continue to bring to market across the full stack

of PCs, compute and storage.

We have had a strong run of announcement since our last call. At GTC, we marked the two-year anniversary of the Dell AI factory with NVIDIA

and extended our leadership in accelerated computing. We introduced new infrastructure across NVIDIA’s Vera Rubin rack-scale platform, the

Rubin GPU architecture and RTX GPUs with form factors that scale the AI factory from the largest clusters in the world to the flexibility and

efficiencies enterprises need. We also extended AI to the desktop with the new Dell Pro MAX systems supporting the GB10 and introducing the

industry’s first OEM desktop with GB300.

At Dell Technologies World, we built on that momentum with new deskside server, storage and data management innovations. — our deskside

Agentic AI solutions help enterprises run production-ready AI locally, supporting use cases like coding, research and secure private assistance

while keeping sensitive data and IP on-prem. Building on strong demand of our integrated rack scale systems, where Dell is the top rack scale

infrastructure provider, we expanded the portfolio with the launch of Dell Power Rack, a turnkey factory integrated solution designed to

accelerate deployment across compute, networking and storage.

In servers, our 18th generation of PowerEdge server portfolio expand support for AI, HPC and enterprise workloads with new air cooled systems

that improve compute density and efficiency. On the data side, advancements in the Dell AI data platform help customers make enterprise data

ready at scale with stronger orchestration, faster indexing of unstructured data and improved analytics performance. We further strengthened

the storage foundation from modern and AI workloads. PowerStore Elite delivers up to 3x performance and density than prior generations with

an industry-leading 6:1 data reduction guarantee. Object scale adds higher-density object storage and PowerFlex extends our exascale storage

architecture with a unified approach across block, file and object workloads.

We continue to expand the Dell AI factory ecosystem with partners, including NVIDIA, Google Cloud, OpenAI, SpaceX AI, ServiceNow, Palantir,

Mistral and CrowdStrike. For example, with Google Distributed Cloud, we are bringing Gemini models on-premises with confidential computes

that customers can run AI closer to the data while meeting data residency, privacy and sovereignty requirements. The bottom line, Dell is

expanding the AI factory from the data center to the desk side across compute, storage, networking, software and services. We’re giving

customers choice, helping them protect their data and enabling them to move from pilots to production faster. With that context, let me walk

you through what we’re seeing in the business.

Our Q1 results. In AI, the opportunity remains exceptionally strong, underscored by durable broad-based demand. In Q1, we booked $24.4

billion in AI orders and recognized $16.1 billion of AI server revenue. We exited the quarter with a record $51.3 billion of AI backlog, and our

pipeline continued to grow sequentially and remains multiples of our backlog, even after converting $24.4 billion into orders. Demand

continues to exceed supply with memory as the primary constraint and we expect to exit the year with meaningful backlog. Our customer count

surpassed 5,000 with growth across neocloud, sovereigns and enterprise customers. Our differentiated offering continues to resonate and our

expanding platforms and capabilities are supporting continued share gain.

We believe those share gains are rooted in things that have long differentiated Dell, strong engineering and design, the ability to deploy and

install at scale, ongoing services and support and flexibility financing and consumption options.

In AI, those advantages matter even more. Customers were not just buying components, they are looking for integrated solutions they can put

into production quickly on infrastructure they control with the performance, security and data foundation their workloads require. Moving to

traditional servers, revenue was up 92% as demand remained well ahead of supply in Q1 with strength across every region. The majority of

demand was driven by large enterprise customers refreshing their compute environments and expanding capacities to support growing

workloads.

For many large customers, ensuring compute availability to modernize and grow remains their highest priority. Customers are also increasingly

focused on infrastructure density as they optimize both spent and data center space which is driving demand and platforms that deliver more

compute capacity, greater efficiency and better consolidation within existing footprints.

Additionally, we saw AI inference workloads driving incremental demand for traditional compute. The majority of the installed base remains on

14th generation or older servers reflecting the continued refresh opportunity going forward. The memory uncertainty is driving customers to

proactively secure access to infrastructure across both traditional and AI workloads over longer periods of time. We also continued to execute

the pricing and margin discipline we established in Q4. All in, we remain confident in the demand outlook for traditional servers and our

portfolio is well positioned to capture that opportunity.

Turning to storage. Revenue was up 8% driven by continued outperformance in our Dell IP portfolio. Dell IP delivered a record demand growth

quarter, making our fifth consecutive quarter of demand growth above market. In primary storage, we saw notable strength in PowerMax and

Power Store. We continue to see momentum in the mid-range ecosystem with PowerStore delivering its eighth consecutive quarter of double-

digit demand growth.

In unstructured, we saw strong performance from Power Scale and object scale with three consecutive quarters of growth, including double-

digit in each of the last two quarters. Dell IP storage continues to become a larger mix of Dell storage with its higher margins. And as a result,

Storage delivered strong profitability was a key driver of overall ISG profitability in Q1.

Page 4

May 28, 2026 / 9:30PM, DELL – Q1 2027 Dell Technologies Inc Earnings Call

Turning to CSG. Revenue grew 17%, and we gained share for the second consecutive quarter with broad-based demand led by large enterprise

customers. Commercial revenue grew 18%, our seventh consecutive quarter of growth with demand up for the ninth quarter. Large enterprise

customers continue to refresh with double-digit growth across all regions. We continue to see runway in the refresh cycle with roughly one-third

of the installed base consisting of devices four years or older.

Consumer revenue was up 9%. Our third consecutive quarter of demand growth, supported by continued strength in gaming. Overall, CSG

profitability improved as better expected demand drove higher attach, greater scale along with improved consumer profitability.

In closing, Q1 was a strong start to FY27 and another proof point in the power of our operating model. We delivered record revenue, EPS and

cash flow and continued returning capital to shareholders while executing with discipline in a challenging demand and supply environment

with notable commodity constraints, particularly in DRAM and NAND. Customers have come to rely on Dell during periods of significant

disruption, and we expect that to continue over the course of the year. Our customers are investing in AI infrastructure, modernizing compute,

expanding storage and refreshing PCs to support the next wave of workloads, we are well positioned with our portfolio.

I am proud of the team’s execution and confident in our ability to create long-term value for customers and shareholders. With that, let me turn

it over to David to walk through the financials and our outlook.

David Kennedy – Dell Technologies Inc – Chief Financial Officer

Thanks, Jeff. We delivered a record first quarter, which positions us very well for the year. Execution was strong across the business from supply

chain to sales to pricing driving record revenue, EPS and cash flow, along with continued strong shareholder returns. Total revenue was up 88%

to $43.8 billion. Gross margin dollars grew 57% to $7.9 billion.

Gross margin rate was 18.1%, driven primarily by mix shift to AI servers with AI revenue up nearly 9x year-over-year. Excluding the impact of AI

mix, gross margin rate was up. Operating expenses were up 9% to $3.7 billion. primarily from variable compensation tied to our

outperformance. Importantly, we drove meaningful scale in the P&L, with OpEx down 610 basis points to 8.4% of revenue, the lowest level in

over 20 years.

Operating income grew 154% to $4.2 billion or 9.7% of revenue driven by higher revenue and resilient margins across traditional servers,

storage and CSG. Net income was up 194% to $3.2 billion, primarily driven by strong operating income. Diluted EPS increased 214% to $4.86, a

record. Moving to ISG. ISG revenue was a record $29 billion, up 181%, marking nine consecutive quarters of double-digit or better revenue

growth.

AI server momentum remained very strong. In the quarter, we generated $24.4 billion in orders, $16.1 billion in revenue and ending backlog of

$51.3 billion. Traditional server and networking revenue was $8.5 billion, up 92% and demand continues to outpace supply.

Storage revenue was $4.3 billion, up 8% with strong demand across the Dell IP portfolio. Execution across the Dell IP portfolio was strong. was

another quarter of growth above the market. Unstructured solutions were the fastest growing along with strong demand across primary

storage. ISG operating income was a record $3.1 billion, up 206%, marking eight consecutive quarters of double-digit or better growth, primarily

driven by higher revenue across the business.

Operating margin was 10.5%, and up 80 basis points even as AI service grew nearly 800% year-over-year.

Looking at the key drivers of margin performance. Storage profitability was up with a higher mix of del IP and rate expansion within the

solutions. Traditional server margins remained stable despite a high inflationary environment. AI server profitability was in line with our mid-

single-digit operating income rate target. Taken together, these factors along with stronger-than-expected revenue drove meaningful scale in

the P&L.

Turning to CSG. CSG revenue was up 17% to $14.6 billion. Commercial revenue grew for the seventh consecutive quarter, up 18% to $13 billion.

while consumer revenue increased 9% to $1.6 billion. CSG operating income was $1.2 billion or 8% of revenue.

This performance was driven by stronger commercial revenue and mix, which supported more higher-margin peripherals. And similar to ISG,

this all drove meaningful scale in the P&L.

Looking ahead, we will continue to balance customer demand with supply while driving scale across the business. Moving to cash and the

balance sheet. We delivered a Q1 record cash quarter with cash flow from operations of $4.1 billion. This was primarily driven by sequential

revenue growth and higher profitability. We ended the quarter with $14.1 billion in cash and investments, up $0.8 billion sequentially.

Our core leverage ratio is at 1.2x. We returned $2.1 billion to shareholders this quarter including repurchasing 11 million shares at an average

price of $147 per share and paying a dividend of approximately $0.63 per share. Repurchase activity remains strong, and we remain committed

to our shareholder return framework.

Turning to guidance. Customers continue to prioritize their IT infrastructure needs with an increased focus on securing supply. We expect that

behavior to continue throughout the year. For Q2, our revenue outlook is similar to Q1’s performance. At the same time, we have increased our

expectations for the second half, while maintaining an appropriate level of prudence given that we’re only 90 days into the fiscal year.

Page 5

May 28, 2026 / 9:30PM, DELL – Q1 2027 Dell Technologies Inc Earnings Call

From a profitability standpoint, the pricing discipline and margin stability we saw in Q4 and Q1 continue to hold. Excluding the impact of AI mix,

our gross margin outlook is better than it was 90 days ago, and we continue to expect margin rate expansion through the balance of the year.

For Q2, we expect revenue of $44 billion to $45 billion, up roughly 50% at the midpoint of $44.5 billion. IHG is expected to grow roughly 75%,

supported by $15.5 billion in AI server revenue and CSG is expected to be up roughly 20%. Operating expenses are expected to be down low-

single digits sequentially. Operating income is expected to grow roughly 80%. We expect sequential improvement in ISG operating income rate

while CSG operating income rate moderates to roughly 6% as we balance demand, share and profitability.

We anticipate a diluted share count of roughly 652 million shares. Diluted non-GAAP earnings per share is expected to be $4.80, plus or minus

$0.10, up over 100% at the midpoint.

For the full year, we expect revenue of $165 billion to $169 billion, up nearly 50% at the midpoint of $167 billion. ISG is expected to grow roughly

80%, driven by $60 billion of AI server revenue at the midpoint or approximately 2.4 x year-over-year. Traditional servers expect to grow just over

60%, storage up mid-single digits and CSG to grow low teens. We continue to prioritize margin rate expansion. Excluding the impact of AI mix,

our gross margin outlook is higher than it was 90 days ago and remains up year-over-year.

We expect operating expense dollars to be up high-single digits, driven primarily by variable compensation. At the same time, our

modernization efforts are paying off, simplifying, standardizing, automating and enhancing our operating model with AI, delivering significant

operating leverage with OpEx as a percentage of revenue in the single digits.

Operating income is expected to grow over 55% with improvement both in dollars and as a percentage of revenue. I&O is expected to be

between $1.4 billion and $1.5 billion. Diluted non-GAAP earnings per share is expected to be $17.90 plus or minus $0.25, up roughly 75% at the

midpoint. In closing, we delivered an exceptional first quarter with record performance across revenue, EPS and cash flow. Revenue was $43.8

million, up 88%.

EPS grew 214% to $4.86. We generated $4.1 billion in cash, and returned $2.1 billion to shareholders. The strength of the quarter reflects broad-

based execution across the business, continued momentum in AI and solid performance across the rest of the business. Our portfolio and

operating model continue to differentiate us in a dynamic supply environment, and we remain focused on supporting customers while driving

shareholder value. We are well positioned for the year.

Thank you to the team for their strong execution, and thank you all for your time. Now I’ll turn it back to Paul to begin Q&A.

Paul Frantz – Dell Technologies Inc – Head of Investor Relations

Let’s get to Q&A. In order to ensure we get to as many of you as possible, please ask one concise question. Let’s go to the first question.

Q U E S T I O N S A N D A N S W E R S

Operator

Ben Reitzes, Melius Research.

Ben Reitzes – Melius Research LLC – Equity Analyst

Well, let me say congratulations, guys. I don’t think I’ve ever seen a Dell quarter like this, maybe Michael had one in the dorm room or something

beating expectations. But congrats to you guys. The question that I have is with regard to the inherent level of real demand. when you see

something like this, you think like there could be some pull forward, especially in the traditional servers and the PCs.

But the way you guided for the year, obviously, by taking up the second half would imply that the pull forward doesn’t have much of an impact

stealing from the rest of the year. Can you just go through the puts and takes of the pull forwards in the major segments, please? And how you

came up with still a higher second half?

Jeffrey Clarke – Dell Technologies Inc – Vice Chairman and Chief Operating Officer

Sure. And thank you, Ben. It was a good quarter. It’s been here a long time. It’s a good quarter.

And when we look at the demand environment that we are operating in today, it’s very different than historical — we think of it as several factors

that are driving demand. Clearly, what you said, there is a pulling component there’s a buy ahead. Customers want to ensure they have access to

supply. They’re concerned about raising prices and they’re acting. There’s also a component of we have large installed bases, whether that be in

PCs, where you have one-third of the units that are four years or older.

We were lagging in a Windows 11 refresh and caught up through the quarter against historical refreshes, and we have a large number of 14G

servers in the installed base that need to be upgraded as customers are moving to modernize. . Customers are upgrading their edge, they’re

Page 6

May 28, 2026 / 9:30PM, DELL – Q1 2027 Dell Technologies Inc Earnings Call

upgrading the infrastructure. They’re looking for more capable PCs as Agentic workloads make their way to the edge. They’re looking to

consolidate space, power and cooling to drive efficiency.

Our new 18G servers are a great vehicle to do that with its 13:1 consolidation. And we have — we’re seeing pockets of fundamental new demand.

There’s new demand driven by AI. There’s an AI drag. There’s inference.

And the agentic AI is driving a new marketplace for traditional servers that we haven’t seen before. And then I think the last two are what you

would expect out of Dell are we’re winning. We’re taking share in all three segments. four, if I count AI servers. So all four major businesses, PC,

server, storage, AI servers, taking share, we’re winning.

And then lastly, during these times of supply disruption and a lot of puts and takes in the marketplace. Customers tend to come to Dell to look

for a calming hand looking for help, and we’re certainly helping as many customers as we have. That’s in PCs, that’s in servers, that’s in storage.

So those are the demand levers of the demand dynamics that we see across all of the businesses. As we look at our forward-looking pipelines,

the pipelines have never been healthier.

They’re actually growing at greater than historical rates, which gave us confidence to raise the guide by $27 billion of revenue for the year. I

hope that helps.

Operator

Mark Newman, Bernstein.

Mark Newman – Sanford C Bernstein & Co LLC – Analyst

Thanks for taking my question. And congrats on a great quarter. we’ll be glad to get a bit more clarity on the breakout of growth between units

and pricing, particularly for the low outperformance we had on traditional servers and just like adding to some of the stuff you said in previous

question, just trying to get a better sense for how much confidence you have that this is sustainable beyond just one or two quarters, but

through this year and into next year. Thanks so much and congrats again.

Jeffrey Clarke – Dell Technologies Inc – Vice Chairman and Chief Operating Officer

Thanks, Mark. Very specifically, we grew units in PCs. The last reported quarter, we grew units in consumer PCs and commercial PCs and

obviously, the aggregate market. We took share. So there’s a baseline of growth there.

We were already the industry leader in PC revenue. And clearly, the inflationary environment has driven up prices. And where we saw that

primarily is on high price band products. and we were the market leader in high price band in PCs, and that expanded as prices moved up. I

won’t parse out the specifics, but we had a great growth quarter in units obviously, the inflationary environment we had the execution towards,

for example, high-end and gaming and consumer.

We had high-priced bands and commercial PCs. And don’t forget the attached business. . The attached business for us around peripherals and

around services is very healthy when the base business grows, it drags more revenue with each and every unit. On servers, absolute server unit

growth occurred.

They’ll probably kick me under the table here. We had significant unit growth in traditional servers. And then we had the content growth. We are

continuing to see on a year-over-year basis more cores, more DRAM, more NAND placed in each and every server. So you have the uplift of more

content.

And then obviously, that content is growing as well in terms of the inflationary side. So absolute growth in units, absolute growth in the content

driven by modernization and consolidation as customers are looking to upgrade and modernize their fleets and then we had the inflationary

part.

The other part of servers that I think is important to call out is this notion of AI drag and seeing traditional servers move and take on AI

workloads. — those AI workloads we’re seeing with very dense servers, making their way into the neo clouds into some of the more advanced

enterprise users think semiconductor companies, big tech that are using it to actually drive some of the inference workloads and agentic

workloads inside their environment. So that’s how I capture it.

Mark Newman – Sanford C Bernstein & Co LLC – Analyst

Thanks very much. Really appreciate it.

Jeffrey Clarke – Dell Technologies Inc – Vice Chairman and Chief Operating Officer

Page 7

May 28, 2026 / 9:30PM, DELL – Q1 2027 Dell Technologies Inc Earnings Call

You’re Welcome

May 28, 2026 / 9:30PM, DELL – Q1 2027 Dell Technologies Inc Earnings Call

Operator

Amit Daryanani, Evercore.

Amit Daryanani – Evercore Inc – Equity Analyst

Thanks a lot for taking my question. Congrats on a really nice set of numbers over here from my side as well. you folks talked about maintaining

an appropriate prudence, I think there’s the way you framed it, like maintaining appropriate prudence when it comes to your guide despite

raising the back half outlook. If I sort of think about H2 versus H1 math for a second, right? I think the guide implies 48% of the revenues this year

will come in the back half of the year. Historically, that number has been around 52%.

Can you just touch on how much of that H2 drop you’re expecting right now versus historically is from a pull-in versus you folks that perhaps

just being a bit more conservative? And is that conservativeness coming more from lack a component availability? Or where could that level be?

Jeffrey Clarke – Dell Technologies Inc – Vice Chairman and Chief Operating Officer

You bet, Amit. I’m going to lead and David’s going to punch the answer home, but I’m the problem. We have a supply issue. We are supply

constrained in the second half. It is not a demand issue for us.

David Kennedy – Dell Technologies Inc – Chief Financial Officer

Yes. I mean that’s the story here. The demand continues to outpace the supply. That demand is broad-based, as Jeff said. So it’s going beyond

the GPU and there’s more AI opportunities from a CPU perspective, traditional server in the PC.

We continue — obviously, these are complex designs. And as we go forward, we’ll continue with operational execution to work with our supply

chain teams, our go-to-market teams and our product teams fully execute and match up to the best execution wise, the supply that we have

with the demand shaping that we see, the teams have obviously executed that tremendously in Q1. And we’ll look to do the same as we head

into the back half of the year. But the demand is there. As Jeff said, that’s what we’re looking at.

We’ll continue to look for more supply, we would like more supply, but the team will continue to go execute and go chase the pipeline that Jeff

referenced earlier, which continues to be in very healthy shape.

Paul Frantz – Dell Technologies Inc – Head of Investor Relations

Thanks, Amit

Operator

Wamsi Mohan, Bank of America.

Wamsi Mohan – Bofa Merrill Lynch Asset Holdings Inc – Analyst

Yes, thank you so much. Very impressive set of results here. I guess if we think about the comment you made on the call, I think you said

customers are prioritizing securing supply, and that is something that you expect will continue for the remainder of the year. In this kind of an

environment where you just noted that demand is extremely strong. What’s your take on the magnitude of the variation in IT budgets for this

year? And do you think that some of this is coming out of the budget for next year as well on the enterprise side.

And I’m also curious, on the traditional servers, I think, Jeff, you mentioned how agentic AI is maybe changing the usage. Is there a materiality of

those to Tier 2 CSPs as well? You noted enterprise strength, but kind of curious if Tier 2 CSPs could be a potential offset to maybe any change in

linearity of demand at enterprise.

Jeffrey Clarke – Dell Technologies Inc – Vice Chairman and Chief Operating Officer

I mean, Wamsi, I can’t speak to next year and budgets for customers. I mean clearly, the longer-term conversations we’re having with customers

are multi-year in nature, of how they secure supply to provide their growth and upgrade their infrastructure and the discussions are multiyear in

Page 8

May 28, 2026 / 9:30PM, DELL – Q1 2027 Dell Technologies Inc Earnings Call

nature. Think three, four, five years. Those discussions are underway. And it really is about access to supply because quite honestly, I can’t tell

them what the price is going to be.

But it’s arrangements and agreements that we’re working with large customers to ensure they have what they need to grow their businesses.

And we saw that occur across some of the largest enterprises around the world.

And our pipelines indicate that’s going to continue but the next set of customers and the next set of customers before that, which is breaking

the historical norms of pipeline build within the quarter and the out quarters. Our pipelines are good two quarters out. And what was really

interesting about traditional servers as an example, is we saw the pipeline grow in quarter greater than historical norms. And we saw the two

quarters out pipelines grow, and it’s showing more customers looking to get access to the technology. We’re seeing budgets grow.

We’re seeing budget shift. Obviously, we’re one quarter into the year. We’ll see how the second half plays out. I think that’s part of the prudence

that we’re trying to convey of where is the demand signal. But the demand that we see continues to be robust.

And we and the supply chain have to go find more parts for the businesses and for our customers to fulfill that demand. I hope that helps.

David Kennedy – Dell Technologies Inc – Chief Financial Officer

I’d add maybe a couple of things, Jeff. I think as we talk about demand outpacing supply in that environment, we would expect to exit the year

with meaningful backlog as we enter next year. So I think that’s an important point. The other piece would be from our financing and DFS

element, which again is a competitive advantage for us. We’re engaged with many customers who in normal course of business would not need

to take advantage of financing offerings for the opportunity to partially use our facility to get as much gear in their environments in year to

manage their potential budget issues is a great way to balance that, and we’re seeing double-digit origination growth across our CSG business,

our traditional server business, our storage business as well as AI which you’d expect.

So we’re seeing different ways we can help our customers get as much technology into their environments as quick as we can.

Operator

Katherine Murphy, Goldman Sachs.

Katherine Campagna – Goldman Sachs – Analyst

Thank you for the question. I was wondering if you could further talk to the raised full year guidance for AI servers to $60 billion and where

across your customer base, the 5,000 customers you mentioned, you’re seeing that $10 billion of incremental opportunity for the fiscal year?

And as a follow-up, how much capacity can you support in the server space with your current manufacturing partners?

David Kennedy – Dell Technologies Inc – Chief Financial Officer

Yes. Look, a strong start to the year, Katherine, $16.1 billion of shipments, $24.4 billion of orders. Our backlog now sits at $51.3 billion, just 90

days into the quarter, we’re raising our full year guide by $10 billion. We’ll continue to work through those deployments as we match up our

supply. Obviously, these are complex designs that we’re engaged on.

We’re actively involved in the technology transition as we get ready for Vera Rubin and obviously, working with all these customer bases in

relation to data center readiness and making sure they can receive the product. I guess, as you look at our portfolio, look, it’s expanding and

growing across all our verticals, whether that’s neoclouds, our sovereign relationships, our enterprise customers, — you would have heard

Michael last week at Dell Tech World talk about our 5,000 customers, which is up over 50% in the last six months.

So you can see the traction that’s coming. And I guess the other data point I’d add is as we look at our pipeline over the next five quarters, that’s

multiples of our backlog, and it’s growing across each individual vertical there again, across neoclouds, individually, sovereign individually and

the enterprise space. So it’s broad-based and it’s present either geography-wise or vertical-wise.

Paul Frantz – Dell Technologies Inc – Head of Investor Relations

And on capacity?

Jeffrey Clarke – Dell Technologies Inc – Vice Chairman and Chief Operating Officer

Yes, I mean, we have the capacity. There’s no capacity issue. It’s parts, supply.

Page 9

May 28, 2026 / 9:30PM, DELL – Q1 2027 Dell Technologies Inc Earnings Call

Katherine Campagna – Goldman Sachs – Analyst

Thank you.

Operator

Samik Chatterjee, JPMorgan.

Samik Chatterjee – JPMorgan Chase & Co – Analyst May 28, 2026 / 9:30PM, DELL – Q1 2027 Dell Technologies Inc s Call

Hi, thanks for taking my question. Congrats from my side as well on the strong results here. Maybe just to focus on one specific comment that

you made in your prepared remarks where the gross margin outlook for the year, ex-AI, is better than you had 90 days ago. If you can just flesh

that out a bit more in terms of is that a function of price increases that you’ve been able to take? Or is that a function of the kind of sort of mix of

products that you’re now selling or where customer demand is focused relative to what you envisioned 90 days ago. Just curious to hear what’s

driving that better outlook there?

David Kennedy – Dell Technologies Inc – Chief Financial Officer

Yes. Sure, Samik. I think it starts with our Dell IP storage portfolio. We’ve taken up our revenue guide, not only for Q2, but also for the back half of

the year. We’re seeing our Dell IP portfolio resonate in the marketplace, whether that’s the unstructured product from a PowerStore perspective

in the midrange.

All of that obviously drives from a Dell IP mix perspective, tailwinds from a margin perspective and a rate perspective. On the other elements of

the business, both CSG and traditional server, we’ve made the commitment to make sure we sustain our margin rates. We see a path to that. We

will continue to manage that as we see the growth. And you put that basket of goods together from a core business perspective, and you see

the lift in the overall margin rate as a result.

Operator

Asiya Merchant, Citigroup.

Asiya Merchant – Citibank Cameroon SA (Douala Branch) – Analyst

Great. I’ll add my congrats here, too.

Thank you for taking my question. If we could just talk a little bit about the attach rates that you’re seeing for the AI servers, especially as you’re

talking about radar enterprise demand here. You talked about 5,000 customers, now that’s up from where it was a quarter ago. If you could just

flesh out how you’re seeing that attach rate for storage and services?

And is that — is there a recent uptick in Dell IP storage a function of attached to AI servers as well as on services, if you could just comment on

that and how that fleshes out into the margin outlook for AI servers? I think I heard maintaining a mid-single-digit margin outlook for AI servers.

Thank you.

Jeffrey Clarke – Dell Technologies Inc – Vice Chairman and Chief Operating Officer

Sure. A lot is into this question. We’ll start with the broader topic. We are increasing the amount of storage and services that we’re providing AI

customers. Period. Michael made reference at Dell Technologies World last week with our unstructured data solutions, the portfolio of products

and how we had won across several major customers, which I think are important bellwethers of what’s changing in the marketplace and how

our products are being perceived.

We are making progress with our AI customers, neoclouds, sovereigns, the high-frequency traders and some of the biggest technology

companies in the world, semiconductor companies in the world, where we are selling more storage, more Dell IP stores, in fact, only Dell IP

storage. And you’re seeing it in our work. Our unstructured portfolio of products had its best quarter in demand ever. Unstructured data is the

dataset that feeds to beast so to speak in AI, and that’s where we’re seeing the greatest growth and making the most traction. If you think about

the portfolio broadly, David mentioned five straight quarters of growth of Dell IP.

It’s five in PowerMax, it’s nine in PowerStore, four in PowerScale, it’s three in ObjectScale, and our Data Protection product is two. We are seeing

the entire portfolio gain momentum, a combination of more competitive products, products designed for the AI era. I would point to Lightning

as being an example of an AI parallel file system, specifically designed for this class of devices and customers.

Page 10

May 28, 2026 / 9:30PM, DELL – Q1 2027 Dell Technologies Inc Earnings Call

We’re seeing increased traction. We’re certified across NVIDIA stack, which certainly is driving. We are engineering with them and how to make

data ingest in data management and the whole data estate easier for enterprises to adopt to accelerate their AI needs.

And quite frankly, we’re in an era where architecture matters more than it ever has. I think of our PowerStore Elite product. We get really excited.

We had fun with this last week at Dell Technologies World. It’s got 3 times the performance of its predecessor, 1.5 million IOPS, 6:1 data

reduction, buy one petabyte of raw storage, store six petabytes of data.

I think about its 70% faster in REITs. It has got 4 times more throughput. I think about the exascale storage we built purposely for this class of

customers. I think about the rack scale architecture that Arthur talked about last week on stage where we talk about the role of storage,

networking compute coming together, driving more performance. I think about what’s happening in the world of data protection where

architecture matters again in 75:1 compression rates.

And then ultimately, our fundamental architecture that drives fewer servers and fewer SSDs to store equivalent amounts of information versus

our competitors. All of that is being packaged up and presented to our entire customer set and then specifically targeted to our AI customers.

Again, whether it’s sovereign, whether it’s neocloud or an enterprise, and we’re seeing traction. Optimistic, not claiming victory here. We have a

lot of work to do.

We’re committed to the space. If you look at the payload that we delivered at DTW last week, it was the biggest and broadest storage payload

we’ve ever brought out at any given time. and there’s more to come.

Using AI inside our R&D organizations, we are delivering larger payloads in shorter periods of time, and storage is the primary vehicle to deliver

that through. So I hope that gives a sense. And obviously, we’re still seeing one of the differentiators we have in the marketplace is services, our

ability to deploy service product, keep up times greater than anyone else, continues to be a differentiator in the marketplace, and we’ll continue

to invest in that broadly across all customers.

Operator

Erik Woodring, Morgan Stanley.

Erik Woodring – Morgan Stanley – Analyst

A big congrats from me on the quarter, just an amazing result. I realize we’re having a lot of conversations here about sustainability. But I’d love

to maybe ask you, if we could go back to last October and knowing what you know now about the market in incremental agentic and ways that

traditional servers are being used perhaps in different ways and your ability to take share from peers. If we went back to the October Analyst

Day. How would you change that 7% to 9% revenue guide and 15% plus EPS guide?

And ultimately trying to get understanding the sustainability of what you’re seeing across multiple years. Which I realize you might not have

numbers, but would just love your thoughts on where maybe that 7% to 9% and 15% plus would go, knowing what you know today.

David Kennedy – Dell Technologies Inc – Chief Financial Officer

Yes. I don’t think we’d work a five-year program on the Q1 earnings call, obviously, as we kind of go through. What we’ll do is obviously validate

what we’re seeing. We were very keen on the back of the Q1 momentum that we see where the growth is real, it’s durable, it’s accelerating, it’s

more broad-based. It’s expanding beyond the GPU. All of those proof points, as they evolve and emerge, give us and gave us the confidence not

only to take up our Q2 guide, which pretty much mirror images what we did in Q1. But also look at the second half and build out incremental

guidance across every LOB, whether it’s PCs, servers, storage and AI as we do that. Jeff touched on earlier, we’re always pretty confident as we

look out over a two, two and a half quarter lens in our pipeline as we do that.

The other, obviously, dialogue there as we talked about an AI pipeline over the next five quarters, building out multiples of our backlog.

So all of those, again, indicate that strong reference points of broader-based demand element and obviously, core to that, it will be the agility for

our EPS over time. So that said, like I said earlier, we’ll look to drive meaningful backlog as we exit this year and I think that’s where we are, Erik, in

terms of looking out any horizon for now.

Jeffrey Clarke – Dell Technologies Inc – Vice Chairman and Chief Operating Officer

Eric, I might add the following perspectives. I don’t think applying historical models or historical views about the market and how it’s going to

act are appropriate today. We’re finding new uses. I mean, the way that I get asked this or I’d ask you this, is what’s the value of adding

intelligence into every workflow, every decision, every product every customer interaction. I would assert the value is pretty darn high.

Page 11

May 28, 2026 / 9:30PM, DELL – Q1 2027 Dell Technologies Inc Earnings Call

And that’s what’s been really, I think, the game changer since that October time is what’s really happened in agentic. And what you’re seeing are

new categories of TAM expanding, you had the three microprocessor leaders talk about an expansion of CPU TAMs. Why? It’s driven by agentic.

What’s happening in agentic? It’s really the movement of AI from an advisor to an operator.

It’s actually going to do something now. It’s going to do something meaningful. But to do something, that agent needs support, just like a

human need support. That agent needs support, in this case of a CPU, you have all of this wonderfulness that a GPU drives. But you have this

work that has to be done around I/O, around branch, retries, managing state. They’re very sequential. They’re very serial in nature as a result of

that. That’s a workload that’s for the CPU.

So if you think about this notion, that’s generally called the harness. So if you think about that harness, the CPU runs it. It’s going to make those

calls. It’s going to manage memory. And it’s in the loop and every decision that an agent makes.

I didn’t — we didn’t know this in October. This is a completely new marketplace. That’s being driven by putting intelligence in every workflow

and every part of knowledge work on the planet today, and we’re just beginning.

Another way to describe this is — the premium for computational capability, whether that be on the edge with a PC, smartphone, servers

running this harness, GPUs doing magical, wonderful work, creating all of this great value, just continues to grow at a rate we’ve never seen, and

it’s pulling the rest of the ecosystem. That’s what we see. And if I go from the trifecta here, all of that stuff has got to be stored. It needs high-

performance storage to be able to ultimately have a receipt of what the agent is doing. So it can be corrected.

You can understand what it did. That’s where we’re at. I don’t know how we would have predicted that in October. And today, I can’t sit here and

tell you how big the TAM is other than I know it’s bigger, it’s growing, and we’re in the early innings of it.

Erik Woodring – Morgan Stanley – Analyst

Thank you.

Operator

David Vogt, UBS.

David Vogt – UBS AG – Analyst

Great. Thanks guys for taking my questions. Jeff, I appreciate all the detail and David on servers and storage. I want to ask a question on CSG.

Obviously, strong performance, taking market share. Can you expand on sort of how you drove profitability dramatically both sequentially and

year-over-year? Kind of going back and thinking through like the best margin I’ve seen in sort of the PC industry, it was probably not 8%.

So just given sort of the drop-through, it looks like over 25% drop through, how do we think about what’s driving that? How much is price versus

maybe low-cost inventory? And how do we think the PC margins trends longer term? Do we go back to your normal historical long-term range

that you talked about at the Investor Day? Or just how do we think about kind of where the market is in your competitive positioning from a

pricing and margin perspective.

Jeffrey Clarke – Dell Technologies Inc – Vice Chairman and Chief Operating Officer

Look, David and I will tag team this. I think the way to look at this, clearly, we benefited from tremendous scale in the business. mean David

made reference that the operating expense as a percent of revenue was down, I believe, 300 basis points on a year-over-year basis.

David Kennedy – Dell Technologies Inc – Chief Financial Officer

Actually a sequential basis Yes, $600 on a year-over-year basis, on a sequential basis, $300.

Jeffrey Clarke – Dell Technologies Inc – Vice Chairman and Chief Operating Officer

Well, that’s powerful in a business like the PC business. We also told you in our last earnings call, we were purposely late in making a price move

because we wanted to build momentum with volume we did. We took share in Q4. In Q1, we purposely moved the price in earlier as we got our

Q2 cost. I think about what we’re doing today, we probably move a little too early in retrospect.

We saw the temper a little bit of demand in the transactional business, I think a consumer, small and medium business. And we’re looking to find

the right optimum place for that, which is reflected in our go-forward guidance of operating margins for the PC business.

Page 12

May 28, 2026 / 9:30PM, DELL – Q1 2027 Dell Technologies Inc Earnings Call

I mentioned we had TRU uplift, TRU uplift drives more profit. I mentioned that we had greater peripheral attach and service attached that drives

profitability of the business. That’s the package. We are not operating at COVID margins. Far from it, in fact.

And if you go back to the operating margins in that era, they were at this range or slightly better. We’re benefiting from the tremendous scale of

the Dell Company, a discipline in pricing that we’re working to find the right optimum balance, particularly in that transactionally oriented side

of the marketplace, consumer, small and medium business. Large deals are done priced deal by deal. And — we like what we’re doing.

We think we don’t have it perfect yet, still trying to find the right balance, but I’m optimistic.

Operator

Tim Long, Barclays.

Tim Long – Barclays Services Corp – Equity Analyst

Thank you. A two-parter, if I could, hopefully, both quick on the more traditional enterprise business. First, you talked a lot about storage. Just

curious with traditional server guided to 60% for the year and storage mid-single digits. Does that mean that we could see a longer pull-through

or tail to storage as we look out a little bit further? And then secondly, you guys navigated the price increases very well.

You’ve touched on that as well. Just curious, in your past history with this, if we do get another uptick that’s kind of meaningful in the next

several months or quarters, — does it get harder to push pricing through another time? Or is it similar to the dynamic that you think you’ve seen

over the last quarter or two?

David Kennedy – Dell Technologies Inc – Chief Financial Officer

Yes, Tim, I guess a couple of things in there. First, if you look at our guide for the full year, again, I go back to the dynamic that we kind of

referenced earlier. When you look at our second half growth in the plan, it’s still, if you like, inhibited by the supply that we can get. So the

demand is there. The demand is outpacing the supply, that applies to across our ISG business as we look at that.

The other element, and I think we’ve discussed this 90 days ago, as you look at our Dell IP mix in terms of our storage portfolio, we continue to

do that crossover with the historical business. So we get more Dell IP versus third party.

By the end of this year, that stops becoming any relevant element of our bridge in relation to that. So seeing growth in storage on a consistent

basis and building that trend is something that excites us from a P&L perspective as we move forward and as we kind of go execute that piece of

it.

Jeffrey Clarke – Dell Technologies Inc – Vice Chairman and Chief Operating Officer

On the pricing side, Tim, we’re repricing, it feels like every day. And I’m sure our customers feel that pain. Unfortunately, I don’t see that changing

given the world that we’re living in today where you have an inflationary environment, whether it’s fuel, whether it’s raw materials, whether

that’s DRAM, whether that’s NAND, CPUs, we are living in an inflationary environment that is changing at a rate that, obviously, we’ve never seen

before. And everything that we see suggests that continues. There will be a point where some customers, it’s enough is enough and they’ll wait

it out.

And we’re seeing that in some cases. In other cases, we’re seeing an acceleration, the notion of that was called out earlier, where folks are trying

to secure that supply now and over multiple years because it’s going to be more constrained.

Tim Long – Barclays Services Corp – Equity Analyst

Thank you very much.

Operator

Simon Leopold, Raymond James

Simon Leopold – Raymond James Inc – Analyst

Great, thank you. Appreciate it. I wanted to come back to the risk and the supply constraints in that I think everybody understands memory at

this point, but I’d like to get a sense from you as to what other elements or factors are limiting any upside beyond the memory constraint?

Page 13

May 28, 2026 / 9:30PM, DELL – Q1 2027 Dell Technologies Inc Earnings Call

And I’m thinking about things like printed circuit boards, et cetera. Just help us understand sort of the rank orders.

Appreciate it.

Jeffrey Clarke – Dell Technologies Inc – Vice Chairman and Chief Operating Officer

Sure, Simon. Yes. I called out the three that we’re spending a tremendous amount of time on. Obviously, NAND and DRAM, microprocessors if

you went down the list, next, it’s likely hard drives. If you go down the list beyond that, there’s lots of things.

If you look at what’s happening in the semiconductor network, you’re seeing utilization of the trailing nodes beginning to fill at greater rates.

Leading-edge node stuff is full as fully allocated. Lead times are a year. So all of those are pressured, but the most pressure comes across the four

that I described and the first three primarily DRAM, NAND, CPUs. And then hard drives and then ultimately, the basket of goods that sit around

that.

Our supply chain has clearly worked through this.

This is what we do, never run out of parts, got a sales force that’s out selling lots with the demand and pipeline that looks very encouraging that

we tried to convey through the call. We have our work cut out for us to work with our partners to drive more supply and every bit and bite

matters. Every microprocessor matters, and that’s what we all try to do every day.

Paul Frantz – Dell Technologies Inc – Head of Investor Relations

Thanks, Simon. We’ll take one more question.

Operator

Krish Sankar, TD Cowen.

Krish Sankar – Cowen and Company LLC – Analyst

Hi, thanks for taking my question, Jeff. Again, congrats on amazing results. I just wanted to find out on your servers, — is there a way to think

about what is the mix of x86 versus ARM? And does it matter to you? Or is there any margin differential between those two architectures from a

Dell standpoint?

Jeffrey Clarke – Dell Technologies Inc – Vice Chairman and Chief Operating Officer

Traditional servers are x86 today. We’re excited about the opportunity with Vera in the future, particularly as we talk about these advanced

workloads that drive increasingly more computational need running this harness, the CPU, managing the scaffolding around every GPU call is

going to be more performant and there’ll be more choice here more opportunity. We need the relief of microprocessors. So we’re excited about

that. On the GPU side, if my memory serves me right, it’s biased towards ARM. So when you think about the big GB 200, 300, obviously heading

towards Vera, you think about direct liquid cooling the large deployments bias towards ARM.

If you think about enterprise and air, so I think B200, B300, RTX-6000 Pro, you think those x86.

Paul Frantz – Dell Technologies Inc – Head of Investor Relations

Thanks, Krish, and Jeff, we’ll turn it over to you for the close.

Jeffrey Clarke – Dell Technologies Inc – Vice Chairman and Chief Operating Officer

Thanks, Paul, and thanks, everyone, for joining us today. Q1 was an exceptional start to FY27, highlighted by strong execution across ISG and

CSG and continued momentum in AI. As we look to Q2 and into the second half, our pipeline indicates demand is not slowing but accelerating

and meaningfully outpacing supply as customers prioritize securing the infrastructure they need across AI, traditional compute, storage and PCs.

Reflecting that strength, we raised our FY27 revenue and EPS guidance by approximately $27 billion and $5, respectively. We are operating with

discipline in a challenging supply environment, scaling the business and continuing to return capital to shareholders.

We feel very good about our position, our momentum and our ability to create long-term value. Thanks again for joining us today.

Page 14

May 28, 2026 / 9:30PM, DELL – Q1 2027 Dell Technologies Inc Earnings Call

Operator

And this concludes today’s conference call. We appreciate your participation. You may disconnect at this time.