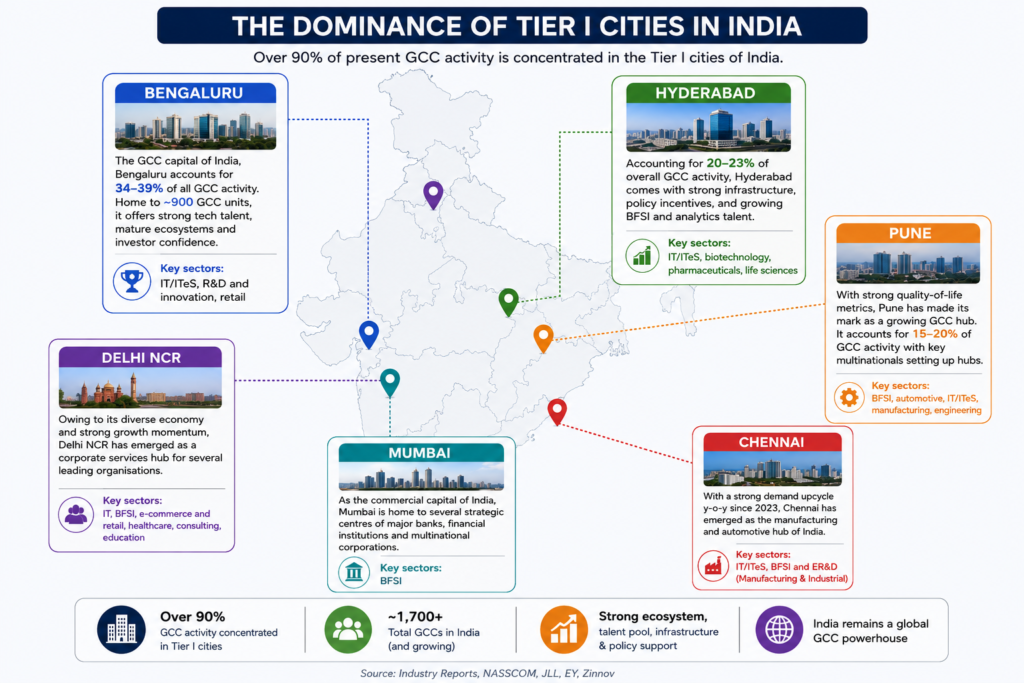

More than 90% of the country’s Global Capability Centre (GCC) activity remains concentrated in its Tier I cities, according to JLL’s The GCC Office Guide report. At the forefront is Bengaluru, widely regarded as the GCC capital of India. Accounting for roughly 34%-39% of total GCC activity and hosting over 900 centres, the city’s dominance is not accidental.

Market watchers believe that Bengaluru’s deep technology ecosystem, mature startup culture and consistent talent pipeline in IT, R&D and innovation have made it the default choice for global firms looking to build long-term capabilities rather than just cost centres.

Close behind is Hyderabad, contributing around 20%–23% of the GCC footprint. JLL in the report said that the city has aggressively positioned itself with strong policy incentives, world-class infrastructure and a growing base of BFSI and analytics talent.

Meanwhile, Pune has carved out a distinct niche with 15%–20% of GCC activity. “With strong quality-of-life metrics, Pune has made its mark as a growing GCC hub,” JLL said in a report, adding key multinationals are setting up hubs in Pune. Some of the key sectors are BFSI, automotive, IT/ITeS, manufacturing and engineering.

The story expands further in Delhi NCR, where a diverse economic base supports GCCs across IT, BFSI, e-commerce, and consulting. Its proximity to policymakers and corporate headquarters adds a strategic layer that few cities can replicate.

Mumbai, the country’s financial nerve centre, plays a more focussed role. While not the largest GCC hub, it remains critical for banking, financial services and multinational corporate functions, leveraging its legacy as the country’s commercial capital.

Finally, Chennai is witnessing renewed momentum. With strong year-on-year demand since 2023, it has emerged as a manufacturing and automotive GCC hub, while also expanding in IT and engineering services.

The Growth of Tier II cities:

Cities such as Kolkata, Ahmedabad, Jaipur, Coimbatore, Lucknow, Mysuru, Visakhapatnam and Kochi are emerging as attractive locations for GCCs seeking to balance cost, talent and resilience. These cities offer 10%–35% lower cost of living compared to Tier I metros, improved infrastructure, state-backed incentives and access to untapped talent pools.