India’s data centre industry is having a moment — and the cables and wires sector is one of its quieter but significant beneficiaries. The push is coming from multiple directions at once. More Indians are online, more businesses are moving to the cloud, the government wants data stored locally, and AI applications are multiplying faster than anyone anticipated. Each of these trends, on its own, would be enough to drive data centre construction.

Together, they are creating a capex cycle that cable manufacturers are well-placed to capture. According to Motilal Oswal Financial Services, the domestic data centre market, currently worth around $10 billion, is on track to grow at roughly 35% annually over the next four years.

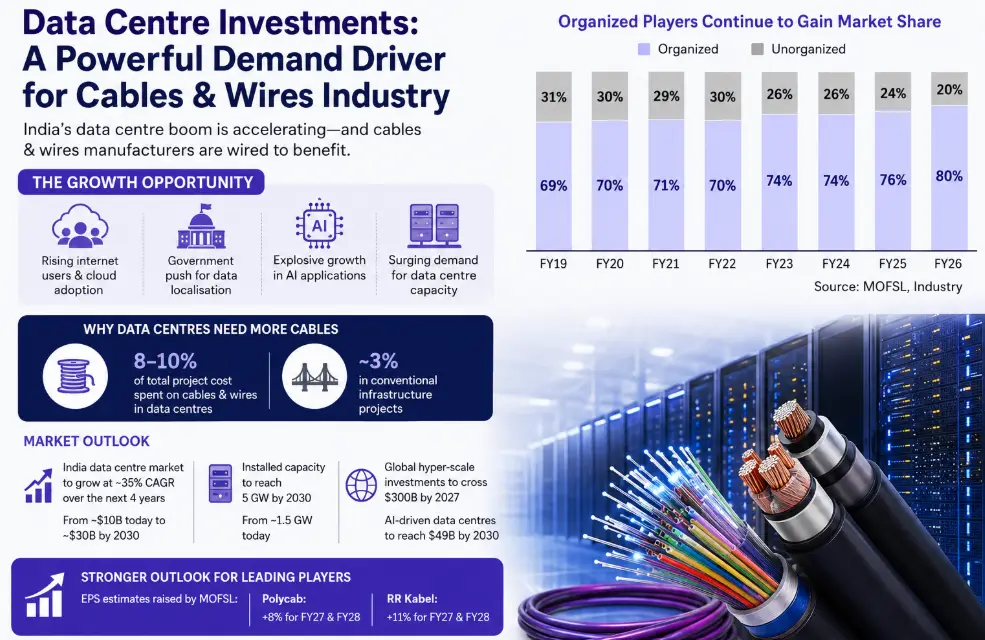

Installed capacity, which sits at about 1.5 GW today, is expected to reach 5 GW by 2030. The reason cable manufacturers are paying close attention comes down to one number: data centres spend 8-10% of their total project cost on cables and wires. That compares with just 3% for a conventional infrastructure project. The gap is wide because data centres need extensive cabling running across power distribution systems, backup infrastructure, cooling equipment, networking hardware and high-speed data transmission networks.

You cannot cut corners on any of it. Globally, the picture is even larger. Annual hyper-scale investments are expected to cross $300 billion by 2027, and spending on AI-driven data centre construction alone is estimated to hit $49 billion by 2030. That means sustained demand for advanced power cables and optical fibre — the kind of specialised product where Indian manufacturers are increasingly competitive.

Motilal Oswal has revised its earnings estimates upward in response to these tailwinds, raising EPS forecasts for Polycab by 8% for FY27 and FY28, and for RR Kabel by 11% for the same period.

The revisions reflect stronger revenue visibility, ongoing capacity additions, market share gains and improving margins. The broader shift in the sector is also worth noting. Organised players now account for 80% of the cables and wires market, up from 69% in FY19. The unorganised segment is steadily losing ground and the data centre boom is one more reason that trend is unlikely to reverse.